Kaspi.kz - Tencent of Kazakhstan

First, apologies. I could not come out with a post earlier. I didn’t find any ideas. But now, I found an interesting portfolio candidate.

Before we get there, I have an observation. Most of the stock-thesis on substack seems to either lack or avoid the level of conviction by the author. I don’t know if they have put their money behind the ideas they write about. And if they did, I don’t know if the author has a 5% or 1% or 10% position. I think that creates a gap for the reader because there is a difference between facts and inference.

Much like our previous posts, I will always tell you how much conviction I have for the ideas I write about and I will only write about what I own or buy. If I write about a stock I am tracking (with a small position), I will inform you. A deal is a deal. :)

With the housekeeping out of the way, let us begin. The company - Kaspi.kz is based out of Kazakhstan and recently IPOed in London Stock Exchange and NASDAQ. The more I dug, the more I liked Kaspi but cognisant of the fact a lot of things could change in the company, country over the next 10 years. So this is a small position (2.5%) in Unfair Portfolio. We are in for the ride and will opportunistically add to this position as the range of outcomes for Kaspi reduces in future.

Summary

Kaspi.kz is the largest super-app in Kazakhstan with 3 key business - Payments, Marketplace and FinTech. Together they touch every, if not most commerce touchpoints for customer and merchants spanning across - banking, loans, deposits, bill payments, P2P, B2B payments, Buy-Now-Pay-Later, Logistics, e-commerce

They have demonstrated an uncanny ability for high-growth and high-profit margins driven by

High customer retention - leading to low net customer acquisition cost

Super-app model - spreading CAC across larger streams of revenue

Low risk, high yield financing - small ticket loans for customers who rarely default (because the loans helps purchase big-ticket products) & these loans funded thro’ customer deposits

Bank, Payments and Retail combined together creates powerful incentives for merchants to provide best service (1/3rd of their sales comes from Kaspi) & customers to purchase and bank with Kaspi (easiest way for purchase & finance it). These customers and merchants stay with Kaspi even though they charge higher fees than peers

All the above is powered by a strong, almost Darwinian culture instilled by CEO Mikhail Lomtadze. Kaspi exclusively measures leadership by Net Promoter Score (NPS) in order to have highest customer satisfation

This has resulted in Kaspi growing topline 30% over last 5 years (FY23 - USD 4.3B) and blended margin of 43%

Kaspi has 14M MAU, of which 9M are DAU (65% DAU to MAU, superseded only by Tencent in China)

Table of Contents

Kaspi.kz - Overview & history

Super Apps - What makes it a strong, defensible business?

Kaspi.kz business model

Risks

Valuations

Further Reading & Listening

Kaspi.kz - Overview & History

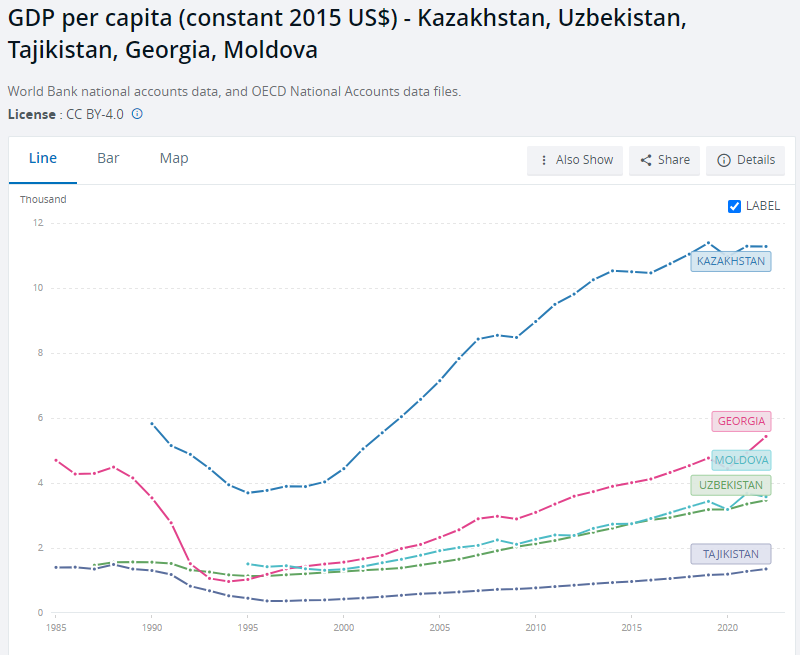

To understand Kaspi, we need to understand Kazakhstan, the last country to get independence from USSR in 1990. As an independent country, it is as old as me. Getting away from its communist roots, Kazakhstan, over the three, decades moved to market-oriented, business friendly country. Their primary growth driver is export of oil, gas & large uranium reserves. Kazakhstan’s annual GDP per capita is close to $11,000 (vs Saudi at $14,000, US at $54,000). They have grown their real GDP at 3.77% growth over last 30 years, much better than their neighbours - Uzbekistan, Tajikistan.

Inflation Adjusted - Real GDP growth

In 1993, Vyacheslav Kim started a household appliance retailer in Kazakhstan, and named it Planeta Eletroniki. In less than decade, Kim made Planeta the largest retailer. However, in early 90s, credit was tough & liquidity was low. Many retailers started to acquire local banks to help finance inventory and customer purchases. In 2002, Planeta acquired Kaspiskiy, a fledgling local bank. By 2007, Kaspi’s banking arm was more commercial with less than 5% as customer deposits. In 2008 during the great financial crisis, Kaspi was squeezed from both sides - bank barely making money and demand for electronics falling off a cliff. Kaspi brought in a Russian Private Equity company - Baring Vostok (spin-off from the Barings Bank in UK!). Partner on this was Lomtadze, a Georgian Harvard Business grad who decided to jump ship and join Kaspi as its CEO.

It is an understatement that Lomtadze made some pivots. Overnight, the legacy leadership was fired. Kaspi Bank decided to move out of commercial business and focus exclusively on consumer side (<5% deposits). They shut the retailing arm, commercial business and quickly got into business of consumer banking, starting with issuing credit cards. Credit cards was their bread and butter.

As part of their strategic push, Lomtadze wanted to make Kaspi customers have the best experience. But in their surveys, they discovered no customer was happy with credit card companies. There were multiple pain points like an opaque fee structure, interest payments, late charges. Overnight, he decided again make a drastic move and kill their main revenue generating business - credit card business.

Kaspi Bank then launched a mobile app, that helped paying bills online for free. This was a game changer in Kazakhstan as most bills back then were paid via banks in-person and banks would charge fees for such bill payments. The app was a raging success. Kaspi Bank renamed itself to Kaspi.kz, quickly starting to launch payments services on top of it - B2B, B2C payments, invoicing, government services etc. They started to take the form of Super App. Before getting into their business, a short primer on SuperApps.

If you are interested a deeper read on Kaspi’s origin story, I highly recommend the 2 articles - The Generalist, Asiamoney