SaaSy no more - Will Claude Code kill SaaS? An investor's guide

The Claude vs SaaS debate boils down to 3 fundamental questions:

What will happen to SaaS Business Model?

Should you sell your SaaS holdings?

Or is it time to back up the truck?

These are the tactical questions to a complex problem. We could endlessly debate the impact of Claude but it means little if that does not answer these 3 questions. The nuanced answer, of course, is that it depends. But..

I think most of SaaS will be eaten by Claude. If not now, it will soon be.

I recently got myself a Claude Pro subscription. It has been blowing my mind every single day. I have a very smart, fast investment analyst working for me 24 hours a day, 7 days a week. Given how much it has improved my investment productivity with the littlest incremental effort, I think SaaS bottom-fishing is a fool’s errand. However the market likes to paint entire SaaS with a broad brush and indiscriminately sell. Lately even data sellers like FactSet, MSCI have come under the crosshairs.

All SaaS are equal. Some are more equal than others

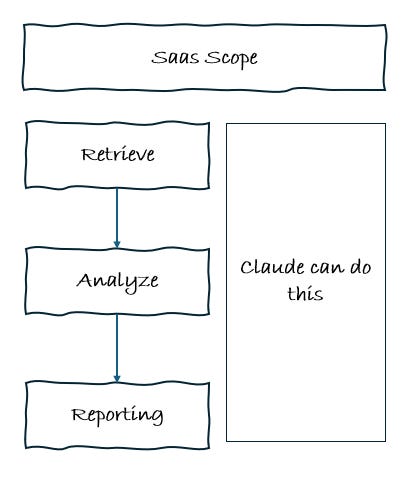

In 90s, when Internet was commercialized, it brought down the cost of sending information from point A to B to zero. If we can send information free, it quickly disrupted all business models that relied on charging economic rent for distributing information - Newspapers, Cable TV, Radio. A good lens to analyse AI disruption is to look for what is being deflated. Claude is bringing down the cost of analysis to zero. So AI + Internet can transport information and analyse it for free. Any SaaS product that analyses information can theoretically be disrupted by Claude. Broadly an enterprise SaaS product will do one or all of 3 things - Retrieve Information, Analyze information and Report it.

Whether this SaaS is vertical focussed one like for accounting or supply-chain hardly matters. The economic rent charged to use that is for 2 reasons - Fixed cost of building it that needs to be amortized and Cost of running it (operations, support etc.). With Claude, the fixed cost of building it is zero (Technically it is $200 per month in license fee. But a far cry from setting up a full SaaS company). When it came to buy-vs-build decision, most enterprise customers would rather buy SaaS earlier even if that meant compromises in feature set, data integrations because it was prohibitively costly to amortize the building cost across a single customer that is themselves. But the building cost has effectively been reduced to zero and if not now, the new players are going to join the game. Microeconomics 101 would tell you if the supply increases, the economic profits would be arbitraged away.

Areas Claude cannot penetrate - Ones with picket white fence

Most of SaaS story began in a similar way - We saw a problem in a specific industry and decided to build software to solve that problem. 99% of SaaS beginnings has the exact same format. If a SaaS company started this way, there is a high chance Claude will steamroll it. The ones on other side of the argument frequently quip about AI limitations, hallucinations etc. forgetting that LLMs are barely 5 years old. The pace of change is unbearably fast. Short term thinking in LLM is thinking about tomorrow and long-term thinking in LLM is thinking about next quarter.

However, some software companies are different. The ones that Claude can replicate in technology but not replicate their product are ones with Strong Network Effects or Proprietary Data. Claude can build another crypto exchange. But it cannot bring liquidity into it like Coinbase. Claude can build an app to transfer money. But it cannot get scale to to subsidise costs for its users like Wise can. Claude can build an app like Uber but it cannot get sufficient drivers in the platform. You see where I am going with this. When there is a question of simple information processing, Claude will kill it. But when the value of the service is from the network or data that is collected over time, it is impossible to replicate it. The software companies that keep getting better with scale is harder to replicate because AI cannot recreate that history.

It is for that reason, I think Adobe, a stock that is a value-investor favourite has a slim chance of survival. Adobe is doing everything that a value investor loves - Using a strong brand and entrenched position to buyback as many shares as it can during depressed prices. But the core product processes and manipulates images and videos. The stickiness comes from a learning curve or familiarity with the product. This learning curve will not stand a chance if a new designer can simply type out what he/she is thinking.

I come back to the point I made earlier - It depends. Claude cannot kill all SaaS. But it will definitely kill most of it. The ones that will survive are the ones that add value not because it is a software solution to a real-world problem but rather they add value through networks, data, infrastructure, or scale. The cost of network building is still very significant even though the cost of technology behind the network can drop to zero through Claude.

Over next few weeks, I will be covering my picks among the SaaS fallen angels. Stay tuned.